For natural gas report week August 26, 2021, the EIA reported a net increase in storage of 29 Bcf. The injection was below forecasts which ranged from 30 Bcf to 47 Bcf and averaged 38 Bcf. In comparison, last year for the same week there was an injection of 45 Bcf and the five-year average is an injection of 44 Bcf.

Working gas in storage was 2,851 Bcf as of Friday, August 20, 2021 per EIA estimates. Inventory was 563 Bcf (-16.5%) less than last year for the same week and 189 Bcf (-6.2%) below the five-year average of 3,040 Bcf.

Natural Gas Market Recap

September NYMEX

12 Month Strip

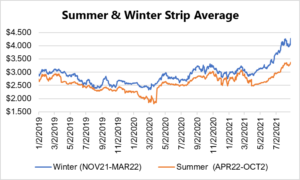

Seasonal Strips

Natural Gas Report – August 26, 2021

Fundamentals

Overall supply averaged 98.9 Bcf/d last week as production increased slightly and imports from Canada rose by 3.7%.

Total demand grew by 0.8% from the prior report week, averaging 91.8 Bcf/d. Residential-commercial use remained steady while power generation demand increased by 2.8%. Meanwhile, LNG pipeline receipts averaged 10.5 Bcf/d, falling 0.2 Bcf/d week over week.

Up to this point in injection season, the average rate of injections is 13% lower than the five-year average. If the rate of injections matched the five-year average of 9.4 Bcf/d, inventory would be 3,530 Bcf at the close of refill season. That’s 189 Bcf lower than the five-year average of 3,719 Bcf.

Natural Gas Prices

Prompt month, 12 Month strip, and the Winter-22 strip (most significantly the lattermost) posted substantial gains over last week. Summer22 movement was more subdued, but at the same time not insubstantial. At the time of publication, September is trading at $4.359/Dth, up 17.5 cents over yesterday’s close. Since September moves off the books today, how much of this is tied to the impending settle and last week’s heat? Probably not much. What evidence do we have it’s related to more long-lasting factors? Keep reading.

DEC21, settled at $4.360/Dth, up 34.1 cents

JAN22, settled at $4.419/Dth, up 33.8 cents

FEB22, settled at $4.331/Dth, up 32.6 cents

MAR22, settled at $4.019/Dth up 26.0 cents

APR22, settled at $3.400/Dth up 14.5 cents

Strips

24 Month, settled at $3.558/Dth up 17.0 cents

36 Month, settled at $3.344/Dth up 12.3 cents

What’s Going On With Prices And How Long Will It Last?

Unlike past weeks where there was a significant correlation between weather and prices, this week has been more dynamic. Let’s take a close look at what happened and how long the impact of each factor may last.

Storage/Production

It’s clear the market reacted to the bullish EIA storage report which disappointed with an injection of 29 Bcf (well below estimates). Before publication of weekly storage numbers, September was trading below $3.900/Dth. By the close of trading, it was up more than 25 cents.

For this week, continued hot weather (even by summer standards) sustained power generation/cooling demand. Anticipation of cooler weather to close out August previously offered hope that the next few weeks would bring sizable injections that could help close the gap between existing storage levels and the five-year average. Instead, this week brought a widening of that gap and the increasing realization we will likely conclude injection season at a deficit.

LNG consumption and production that hasn’t ramped up despite healthy demand also contributed to the storage story this report period. How will all this shape up as we approach winter?

- As a seasonal factor, hot weather will naturally subside for the shoulder season before cooling demand trades off with heating. Should winter bring below-average temperatures, the impact to an already tight supply-demand balance will be ugly.

- LNG exports have doubled last year’s levels. With global LNG prices at historic highs, demand for US supply is expected to max out capacity through 2022. As such, LNG will continue to represent a major demand factor through next year.

- Don’t expect production increases to alleviate supply concerns any time soon. Last year, investors put the skids on new capital drilling projects. Excess supply led to prices that were so low that many producers reported dismal earnings while others filed for bankruptcy. Right now prices are showing some signs of strength, but not enough to reverse course. In fact, the EIA reported, “According to Baker Hughes, for the week ending Tuesday, August 17, the natural gas rig count decreased by 5 rigs to 97 rigs, and it is now at its lowest level in over two months.”

The forecast? Look for supply to average 92.9/Bcf/d throughout the rest of 2021. By injection season next year, higher prices are expected to support production increases. The EIA projects at that point production will average 94.9 Bcf/d.

Weighing weather, LNG demand, and production, the impact to prices will likely persist through winter until production picks up and gives us a little wiggle room. Confirmation of this is evidenced in the Seasonal Strip graph posted above. As Winter-22 prices have continued a steady rise, Summer-22 is no longer keeping pace.

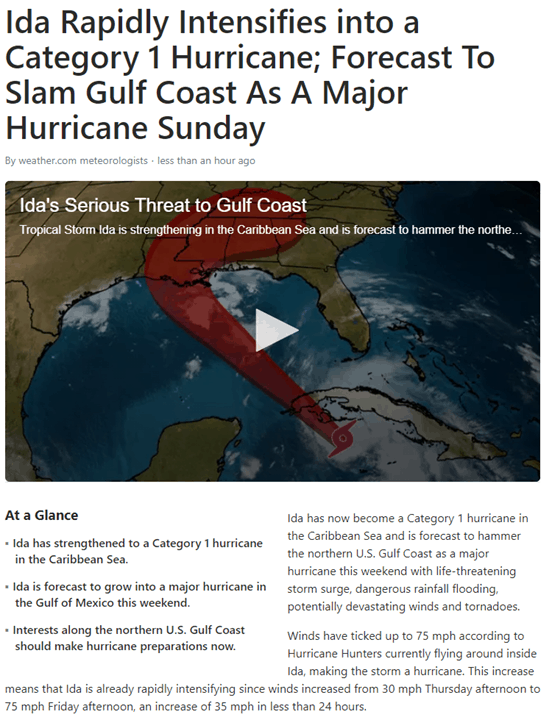

More Weather

This image sums it up.

According to Reuters, “Gulf of Mexico offshore wells account for 17% of U.S. crude oil production and 5% of dry natural gas production. Over 45% of total U.S. refining capacity lies along the Gulf Coast.”

By the time Ida makes landfall, it’s forecast to be a Category 3 storm. As such, “U.S. energy companies on Thursday began airlifting workers from Gulf of Mexico oil platforms and moved vessels ahead of a powerful hurricane forecast for the weekend.”

This stalls production which will clearly impact next week’s storage report, absent an offset from demand. Now would be an ideal time for cooler temperatures. Nonetheless, the impact to prices should be limited…at least for Ida. However, hurricane season runs through November and NOAA predicted an above-normal hurricane season, so don’t dismiss this factor.

Geopolitical Implications

This week’s events in Afghanistan have forced back to attention market reaction following 9/11. Apart from economic shock, natural gas and oil resources were targets of competing factions as they sought control of these resources. Additionally, potential weaponization of oil and natural gas assets made production dangerous. Talk of risk premiums, also known as terror premiums, became commonplace.

Now, as instability once again threatens the region, foreshadows of terror premiums have returned.

Right now, the focus rightly remains on rescue operations. Beyond next week, though, this may become more of an issue.

Read more about this in this Fox Business Opinion piece.

Do you have the best natural gas contract for your business?

We can help you evaluate your current contract and explore your natural gas buying options. Call us at 866-646-7322 for a no-cost, no-obligation analysis today.